EBIT, EBITA, and EBITA are profitability metrics that assess a company’s profitability and operational efficiency, often used for valuation, investment analysis, etc.

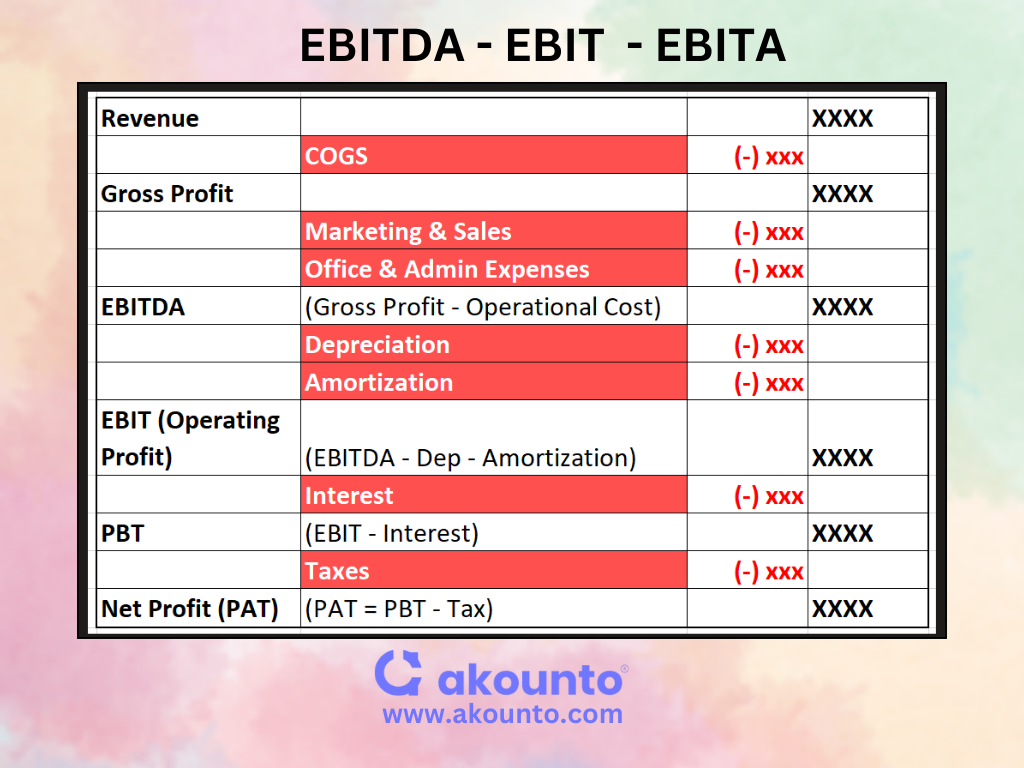

EBIT (Earnings Before Interest and Taxes) and EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) both exclude the impact of interest and taxes from their calculations. The key difference between EBIT and EBITDA lies in the treatment of non-cash expenses, which are “Depreciation” and “Amortization.”

These non-cash expenses do not impact the cash flow statement as they are not paid. Depreciation and amortization occur at a predefined rate irrespective of the business activity thus, they are also non-operating expenses.

When it comes to “interest” and “taxes,” then we need to understand two things:

- Interest is paid on the “debts,” which represent the capital structure of the business. Once the debt is taken, interest is to be paid regardless of business performance. But the difference between “Depreciation and amortization” and “interest” is that interest will be paid and will lessen the cash reserves. Interest payments will be shown in the cash flow statement as “cash outflow.” It is a cash expense, though a non-operating expense, too.

- Taxes are paid to the government and are cash expenditures. Thus, they materially impact the company’s cash position and are thus cash expenses. Though taxes are levied on profits and not part of a business activity, they are also non-operating expenses.

Therefore, “interest” and “taxes” are common and excluded by both EBIT and EBITDA; the difference is due to the treatment of depreciation and amortization. EBITA (Earnings Before Interest Tax and Amortization) is another variation of EBITDA that is most suited when a business has more intangible assets than physical assets.

Reasons for Tax and Interest Exclusion

Tax

- EBIT, EBITDA, and EBITA are on a pre-tax basis.

- Taxes are jurisdiction dependent.

- Some taxes can be due to deferred taxes (DTAs/DTLs) and net operating losses (NOLs).

- Thus, they are non-operating and do not reflect the core business activities of the company.

Interest

- Interest payments reflect the company’s “capital structure,” which is due to management choices and results in capital borrowing costs.

- Even in the same sector or industry, companies can have different capital structures (debt-equity mix to fund the company).

- One company may choose to pay dividends, while the other may keep “retained earnings”. Thus, the balance sheet may reflect different positions, and it will be inadvisable to compare the profitability of the companies where the interest component is deducted to represent profit before taxes.

- Thus, we see that interest payments as non-operating are separate from core business functions.

For comparison purposes, EBIT and EBITDA (its variations) are chosen as they do not take into account the impact of capital structure and taxes. Thus, comparing only the company’s operational performance is possible.

Depreciation and Amortization in EBITDA and EBIT

Depreciation

- It is the charge for the wear and tear of the asset—the obsolescence of assets—which is charged in the company’s income statement. We can call this asset depreciation.

- In the case of EBITDA, once we add back “depreciation,” we nullify the impact of depreciation expense, see the company’s operational earnings, and remove the impact of asset depreciation. In the case of EBIT (operating income), the impact of asset depreciation is already taken into account; thus, EBIT is impacted by a non-cash expenditure.

Amortization

- Amortization is similar to depreciation; the only difference is that it applies to intangible assets.

- The depreciation of intangible assets is called amortization. These assets are trademarks, goodwill, copyrights, etc.

- Amortization is more common in the case of a services company like a software company, which can have many patents.

- Calculating EBITDA involves adding back depreciation and amortization, which again nullifies the impact of non-cash and non-operational expenses. Thus, the true operating performance is given prior to any taxes and interest payments.

Thus, for all the above reasons, investors largely prefer EBITDA for comparisons.

Use of EBIT, EBITDA and EBITA

Many companies separately report GAAP and non-GAAP earnings. A business may be raising capital or disposing of a high-ticket asset in a given accounting period; thus, the GAAP earnings may distort the financial performance, so using non-GAAP financial reporting tools like EBIT, EBITDA, and EBITA, the normal or actual performance is represented.

In the USA, the SEC (Securities and Exchange Commission) does not consider net income, EBITA, and EBITDA as a part of GAAP (Generally Accepted Accounting Principles). It requires the companies to reconcile EBITDA to net income.

A professional investor, stock analyst, underwriter, etc., will like to check a company’s fundamental earning potential before investing, which will be represented by EBITDA. This will make companies comparable as an investment option. A business buyer who may be interested in a leveraged buyout will be interested in a company’s own earning potential through its business model and cash flow situation.

Thus, EBIT, EBITDA, and EBITA are most commonly used for company valuations too.

Interpretation of EBIT and EBITDA

Understanding EBIT

EBIT is also called operating profit. EBIT includes all incomes and all expenses incurred by a company in a given accounting period. EBIT includes both operating and non-operating expenses and also cash and non-cash expenses.

The formula for calculating EBIT

EBIT = Net Income + Taxes + Interest

Or

EBIT = Revenue – Operating Expenses

EBIT is usually back-calculated from the company’s “net income,” which is shown in its Income Statement.

When a firm does not have any non-operating income, then EBIT is also called as operating income.

Understanding EBITDA

EBITDA is a financial metric for comparing companies’ operating performance. To calculate earnings from operations, it excludes the impact of depreciation and amortization, the cost of debt capital, and taxes. EBITDA also excludes all non-cash and non-operational items.

When a company has expensive intangible assets and large fixed assets, the amount of depreciation and amortization is also high. Thus, the resultant earnings after deducting these charges will distort the company’s operational performance. So, creditors, investors, and management prefer to use EBITDA to measure profitability.

The formula for calculating EBITDA

EBITDA is back-calculated from the company’s “net income,” which is shown in its Income Statement.

EBITDA=Net Income + Interest Expense + Taxes + Depreciation + Amortization

Or

EBITDA=Revenueв€’Operating Expensesв€’Depreciationв€’Amortization

Or

EBITDA = EBIT + Depreciation + Amortization

Understanding EBITA

Investors consider earnings before interest, taxes, and amortization (EBITA) a more accurate measure of profitability. It is a further variation of EBITDA, with the change that it takes into account depreciation and not amortization.

EBITA is more suited for comparing service-based companies, consultancies, etc., that have minimal capital expenditure and do not hold large or major physical assets. EBITA can not be used in asset-heavy industries or sectors.

Comparative Analysis of EBIT Vs. EBITDA

| Comparative Analysis | ||

| Basis of Comparison | EBIT(Earnings Before Interest and Taxes) | EBITDA(Earnings Before Interest, Taxes, Depreciation, and Amortization) |

| What does the metric measure? | EBIT measures operating profitability. | EBITDA measures operational performance and cash flow generation. |

| Formula | EBIT = Net Income + Interest Expense + Tax Expense | EBITDA = Net Income + Interest Expense + Tax Expense + Depreciation Expense + Amortization Expense |

| Inclusion of Non-Cash Expenses | EBIT excludes the impact of depreciation and amortization | EBITDA does not exclude depreciation and amortization. |

| Usage | EBIT helps in comparing operating profitability within the same sector. | EBITDA is useful more in asset heavy industries with high capital expenditure. It helps in the assessment of cash flow generation capacity. |

| Sensitivity to Capital Structure | Less sensitive because it excludes interest expenses | EBITDA excludes both interest and debt repayment-related expenses, thus it is less sensitive as compared to EBIT. |

| Evaluation of Financial Health | EBIT provides insight into operating profits before financing and tax payments. | EBITDA offers an evaluation of cash flow generation capacity, which is important for assessing financial health |

How to Choose Between EBIT and EBITDA?

- EBIT is way more simpler as compared to EBITDA. EBIT highlihts only operating performance, EBITDA is more comprehensive and excluded all non cash expenses.

- Another factor is related to the capital structure of the company and impact of debts. Both EBIT and EBITDA excludes the impact of cost of borrowing and give level-comparison field within the same industry. But if you are evaluating only one company for financial performance, investment analysis, or any such matter, then EBITDA is much more preferred than EBITA.

- EBITDA is more preferable in industries with very high capital expenditure, because it excludes depreciation and amortization, thereby providing better view of operational efficiency than EBIT.

- Usually investors preference for a metric and its industry wide usage impacts the choice of metric. An investor may prefer to use one metric over the other.

- Usually EBITDA is used in valuation and multiples or enterprise value (EBITDA ratio). EBIT is only usable in such a scenario when interest expenses can dramatically change in the near future.

- For service sector or industry with very low asset holding, EBIT is preferable over EBITDA.

Use Case Examples of EBIT, EBITDA, and EBITA

EBIT (Operating Income)

- Ratio analysis: Measuring a company’s operational efficiency by calculating the EBIT margin, which tracks the amount of revenue that translates into operating profit.

- Intra-industry comparison: EBIT is also known as operating income and is used to compare companies within the industry. It helps the investors to focus on the efficiency of core business operations to generate cash.

EBITDA

- Company valuation: Valuation metrics like the Enterprise/EBITDA ratio help compare companies and evaluate them before mergers and acquisitions.

- Creditworthiness: EBITDA augments the assessment of creditworthiness w.r.t. Debt service coverage ratio. Creditors and lenders use EBITDA multiples to assess debt servicing capacity and decide on loan conditions.

- Business resilience: EBITDA highlights the efficiency of core business operations to generate profits. For a business to be sustainable, it is recommended that it should be able to fund its own running operations from its core business activities, so that debts are taken for business expansion rather than routine works.

- Risk exposure: Low operational efficiency highlights leaks and mismanagement of funds. The business may have to divert debt financing for day-to-day operations leading to interest payments. This increases the default risk and can lead to a debt burden. Thus, a consistently low EBITDA hints towards unsustainable business operations.

EBITA

- Adjusted earnings: EBITA is a variation of EBITDA and is particularly useful for assessing the operational efficiency of companies that have more intangible assets

Investment evaluation: Service companies grow quickly and can expand easily without needing to spend a lot of money on buildings or equipment. EBITA helps investors see how well the company is doing and how much money it’s making.

Conclusion

Business should be compared and analysed periodically and regularly to know how it is performing in comparison with other industry players. Evaluating business helps you keep a tight control over your finances and processes. Though EBITA, EBITDA, and EBITA are non-GAAP financial metrics, but they provide an operational insight into the business which is often an indirect way to measure the reliance and sustainability of the business. The choice of the metric depends upon what the business user wishes to analyse. If you want to exclude the impact of amortization and depreciation, then EBITDA is the choice, but if you feel that amortization and depreciation do impact the valuation of assets and should not be ignored then EBIT is the right option.

Visit Akounto Blogs and learn more about topics of finance and accounting that are helpful to run your business smartly.